Picture this: your home, built to modern standards, energy-efficient from day one, in a neighbourhood that’s still taking shape. That’s the appeal of a new-build (nieuwbouw) property in the Netherlands. And right now, the Dutch government is actively pushing for more new housing, which means more opportunities for you.

But here’s the thing most people don’t tell you upfront: buying a new-build is not the same process as buying an existing home. The timeline is longer, the mortgage rules work differently, and a few key decisions need to be made early. Get them right and you’re set. Get them wrong and things can get complicated fast.

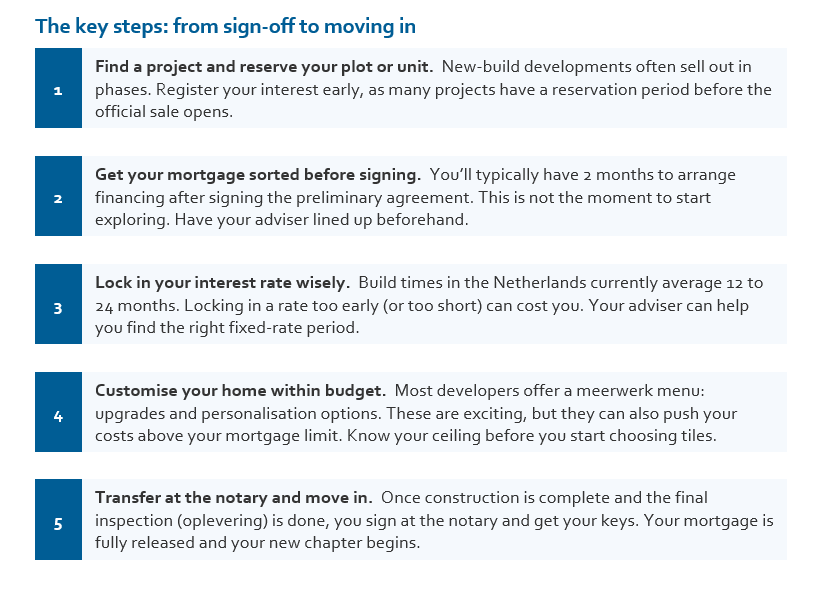

Let’s break it down so you can move forward with confidence.

How does buying a new-build actually work?

When you buy a new-build in the Netherlands, you’re typically signing a purchase agreement before a single brick is laid. This is called a koop-/aannemingsovereenkomst, a combined purchase and construction contract. You pay for the land and the build separately, in stages, as construction progresses.

This is where it gets interesting for your mortgage. Unlike a standard mortgage where you receive the full amount on the day of transfer, a new-build mortgage is released in instalments (termijnnota’s) as each construction phase is completed. During the build period, you only pay interest on the amount already released, not the full loan. That said, you may still be paying rent elsewhere, so planning your cash flow matters.

What’s different for expats?

As an expat, you can absolutely buy a new-build in the Netherlands, but lenders look at your situation differently. Income in a foreign currency, a temporary residence permit, or a shorter employment history in the Netherlands can all affect which lenders will work with you and under what conditions.

The good news? This is exactly our territory. Expat Mortgages specialises in navigating these situations. We know which lenders are genuinely open to expat applications, and we know how to present your file in the strongest possible way.

Loan to value: borrowing 100% of the construction costs

One of the most practical advantages of buying a new-build is how the loan to value (LTV) rules work. With a new-build, lenders will finance up to 100% of the total construction costs, and that includes any additional works (meerwerk) you choose to add. So if you decide to upgrade your kitchen, add underfloor heating, or adjust the layout, those costs can be wrapped into your mortgage, as long as your loan to income (LTI) allows for it.

WHY THIS MATTERS New-build vs existing property: a key difference

With an existing home, renovation costs can only be added to your mortgage to the extent that they increase the property’s appraised value. If your renovation adds less value than it costs, you fund the difference yourself. With a new-build, the entire construction sum is financeable from the start. Your meerwerk choices are not a gamble on added value; they are simply part of the build.

The practical takeaway: work out your meerwerk wish list early, share it with your mortgage adviser before signing, and make sure the total sits within your lending capacity. That way there are no surprises when the bill arrives.

Closing costs and own resources: what you still need to have saved

New-build is often pitched as the cheaper option to get into, and in terms of buyer’s costs, that’s true. You avoid the 2% transfer tax that comes with buying an existing home. Your main upfront costs are notary fees, a translator if needed, and mortgage advice. Compared to an existing property purchase, that is a significant saving.

But here’s where many buyers are caught off guard: the bank still expects you to demonstrate substantial savings before they approve your mortgage.

IMPORTANT TO KNOW You need to show you can carry both rent and mortgage

Because new-build construction typically takes 12 to 24 months (sometimes longer), you will be paying rent while your mortgage interest is already starting to accumulate. Lenders want to see that your savings are sufficient to cover this overlap for the entire duration specified in your koop-/aannemingsovereenkomst. The longer the construction period, the more savings you need to demonstrate. This is not a deal-breaker, but it needs to be planned for well in advance.

The bottom line: come to the conversation with a clear picture of your savings, your monthly obligations, and the expected build timeline. We can then work out exactly what the bank needs to see and make sure your application is as strong as possible.

No transfer tax: a real advantage

New-build properties in the Netherlands are also exempt from transfer tax (overdrachtsbelasting). Instead, VAT (BTW) at 21% is already included in the purchase price. This is often offset by the energy savings a modern, well-insulated home brings, and lenders will factor in a higher mortgage capacity for energy-efficient homes.

Ready to take the next step? Don’t wait until a development launches to start the conversation. The earlier you know your options, the better your position when the right project comes along.

Active New Built projects

Living in The Triplets means living in one of Amsterdam’s most central locations – an oasis of calm in the dynamism of the city. The Oosterpark is just under 10 minutes by bike and the Hortus Botanicus eight minutes away. On the corner, the terraces of Brouwerij ‘t IJ, coffee shops, specialty shops and small boutiques beckon. In the evening, take a leisurely stroll along the water or cycle to Studio K for a film, concert or good conversation at the bar. This is the city at its liveliest – and warmest. Meetings happen spontaneously, in the city and at The Triplets itself.

Park Valley is part of Holland Park. This former industrial site is transforming into a striking residential area with distinctive architecture. Holland Park East and the student campus are nearly fully developed. Construction of Park Valley will begin in the coming years. In total, Holland Park will feature 5,200 homes with a central location close to Amsterdam

In Boomgaerde, you will find the best of many worlds. The dunes and a nature reserve are just around the corner, a 9-minute bike ride away. Charming Westland villages surround you. But all the conveniences of the city are never far away either. Near Boomgaerde, you have everything you need. From a GP practice to a shop, and from a playground to a sports club. For your daily groceries, you can go to places like Monster or Poeldijk. Surfing, horse riding, golfing, swimming, walking, and cycling: all of that is possible in the immediate vicinity of Boomgaerde. Or how about De Uithof a little further away for a round of ice skating or a run on the slopes for skiing or snowboarding? When it comes to physical activity, you will really have a blast here.

The Havenmeester offers spacious, sustainable living with all city amenities within easy reach. By car, you’re only 10 to 15 minutes from the centres of The Hague and Delft, or the vibrant seaside boulevard of Scheveningen. The European Patent Office (EPO) is just a 5-minute journey away.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute personal financial, legal, or tax advice. While we strive to keep our content accurate and up to date, rules, regulations, and market conditions can change quickly—sometimes faster than we can update our articles.

Before making any financial decisions or relying on this information, we strongly recommend consulting a qualified advisor who can assess your individual situation and provide tailored guidance. We do not accept any liability for actions taken based on this content.